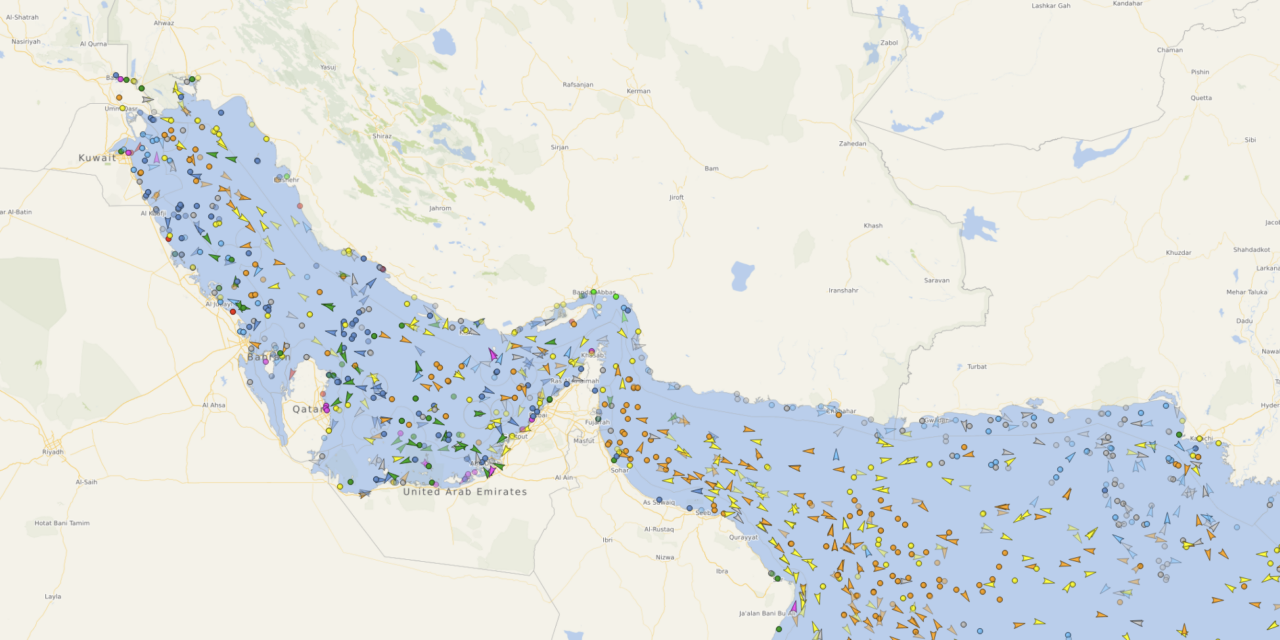

TRIESTE – The risk of a simultaneous disruption in the Strait of Hormuz and the Red Sea, following US and Israeli strikes on Iran, is pushing major carriers back into diversions away from the Suez Canal, with direct impacts on traffic to the Mediterranean, in the form of longer transit times, surcharges and insurance uncertainty. Over the past twelve months, maritime access to the Mediterranean has remained unstable. Asia–Europe and India/Middle East–Mediterranean routes have alternated between cautious returns to Suez and new diversions via the Cape of Good Hope. In late February and early March 2026, the picture became more complex: alongside tensions in the Red Sea, alerts and advisories emerged concerning the Strait of Hormuz, creating a double chokepoint along the corridor leading to Suez. For many supply chains, the key passage remains the Bab el-Mandeb – Red Sea – Suez Canal sequence. When that corridor is avoided, container lines switch to the alternative route around Africa, re-entering the Mediterranean via Gibraltar. Operationally it is safer, but it means more miles, more sailing days and a greater deployment of vessels to maintain frequencies. Communications from the main carriers have been explicit.

Maersk announced the diversion via the Cape for services ME11 and MECL, including the Middle East–India link into the Mediterranean, citing deteriorating security conditions and a suspension of transits in the Hormuz and Bab el-Mandeb area. Hapag-Lloyd diverted the IMX service and introduced a war risk surcharge for cargo to and from the Gulf. CMA CGM instructed vessels in the Gulf area to proceed to safe shelter and suspended passage via Suez, applying an emergency conflict surcharge. MSC communicated security measures for transits and the temporary suspension of bookings to the Middle East. The common message is «safety first»: crew, vessel and cargo come before commercial continuity. In practice, however, these decisions affect access to the Mediterranean.

Mediterranean ports served by Asia–Med or India–Med loops are seeing transit times lengthen and uncertainty increase around arrivals. Even when a route is not formally closed by an international authority, the combination of military risk, operational diversions and limited insurance cover makes the passage impractical for many operators. On the information side, reporting centres such as UK Maritime Trade Operations have described an “highly volatile” environment, with electronic interference and VHF messages about alleged closures that are not verifiable and not legally binding. In parallel, the US Maritime Administration has recommended avoiding the area where possible and maintaining safety distances for certain categories of vessel. Operational guidance includes constant monitoring of official channels and enhanced risk assessments ahead of any transit.

Insurance is another key factor. In early March 2026, several P&I clubs and insurers issued notices of cancellation or war-risk exclusions for areas linked to the Gulf and Iranian waters. Among them were Gard and Skuld, as well as the London P&I Club. In practical terms, even if a route is technically navigable, cover can become more expensive or unavailable at very short notice. This bears directly on voyage costs and on shipowners’ willingness to enter certain areas. The surcharges announced by carriers confirm cost pressure. War risk surcharges and emergency conflict surcharges are being applied to standard TEU and to reefer or special-equipment containers, with differentiated amounts. Added to this are indirect costs: higher fuel burn on the Cape of Good Hope route, more ship-days, possible anchorage congestion at Gulf ports, equipment imbalances and empty-container repositioning. For the Mediterranean, the central issue is the stability of flows via Suez. Even during periods of relative calm, market data have shown transits below pre-crisis levels. The return of services has been selective and cautious, with testing on individual loops and, in some cases, standby tonnage. The new escalation in late February has once again reversed course.

If diversions via the Cape of Good Hope persist, the effects will be visible on three fronts. First, longer delivery times for Asia–Med supply chains. Second, greater volatility in freight rates and surcharges. Third, lower schedule reliability, with potential recourse to blank sailings or loop reconfigurations. It is not possible to confirm a “formal closure” of Hormuz, in the legal sense of the term, on the basis of VHF reports alone. Authorities distinguish between unverified messages and official restrictions. However, from a commercial and insurance standpoint, decisions by carriers and insurers produce an equivalent effect: access becomes riskier, more expensive and less predictable. For Mediterranean ports—including those dependent on Asia–Med and India–Middle East–Med traffic—this opens a new phase of uncertainty. The global network remains operational, but with different geometries.