TRIESTE – 2025 marks a turning point for North Adriatic ports, amid the reorganisation of carrier alliances and the impact of geopolitical crises. This is what emerges from the AIOM analysis, which portrays a system in transition, but still resilient in terms of overall volumes.

A decisive factor was the end of the 2M alliance between Maersk and MSC, formalised in March 2025, and the launch of the new Gemini Cooperation between Maersk and Hapag-Lloyd. The change has reshaped deep-sea services in the eastern Adriatic area: direct calls now mainly serve Rijeka and Koper, while Trieste is served by feeder connections.

Under the new structure, the Ocean Alliance is maintaining direct calls at ports in the area, while MSC, now outside any alliance, is strengthening its own independent services. The group led by Gianluigi Aponte has in fact revised its strategy for Trieste in recent weeks, where the direct Phoenix service has been restored with smaller-capacity vessels, no longer supported by feeder connections to the US East Coast via Gioia Tauro.

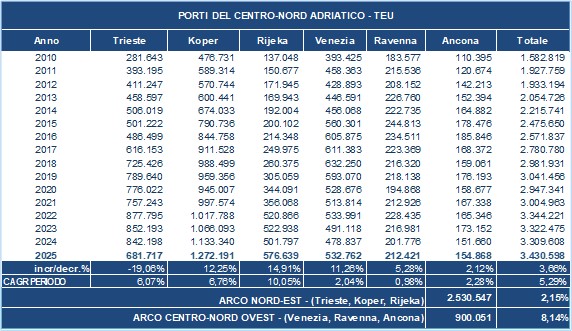

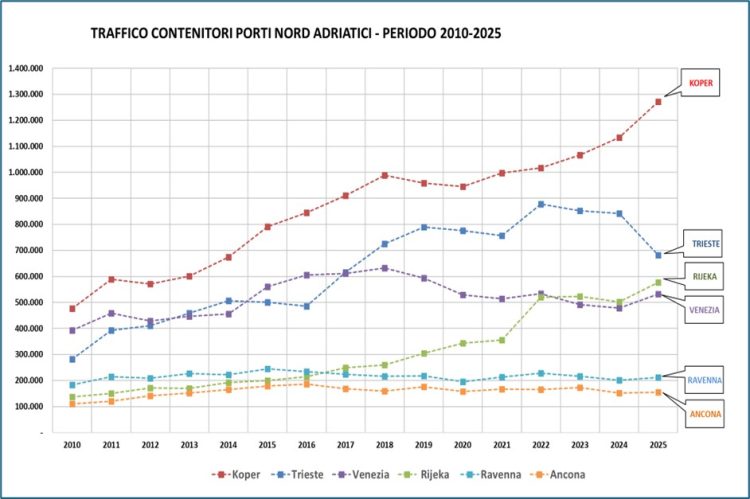

On the traffic front, 2025 shows a differentiated picture. The eastern Adriatic ports are recording divergent trends: Koper and Rijeka are growing by 12.25% and 14.91% respectively, while Trieste is feeling the loss of transhipment volumes linked to Maersk following the end of 2M. Rijeka, in particular, has risen to third place among Adriatic ports and aims to further strengthen its position, despite some critical issues in its hinterland rail connections.

The trend is different for the western Adriatic ports (Venice, Ravenna and Ancona), which in 2025 are recovering the losses recorded over the previous two years, linked to diversions caused by the Red Sea crisis.

According to AIOM, overall the North Adriatic port system should maintain substantially stable traffic levels, although with an internal redistribution of volumes between the various ports. For Trieste in particular, the launch of the new weekly MSC connection could allow a recovery in 2026 estimated at between +6% and +10%, although forecasts remain tied to the evolution of demand and the international scenario.

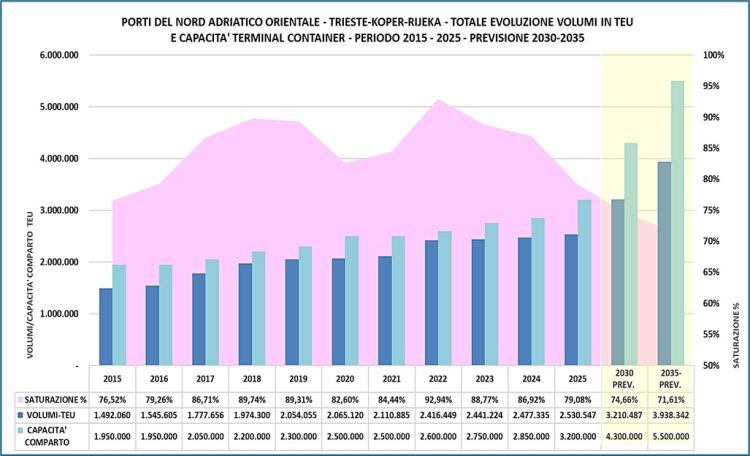

The context remains strongly conditioned by geopolitical tensions, particularly in the Red Sea and the Middle East, a key hub for traffic between Europe and Asia. Despite this, the analysis highlights how the ports of Trieste, Koper and Rijeka are supported by major investment programmes that will increase their capacity in the coming years.

Looking ahead, the North Adriatic system therefore appears able to face this phase of uncertainty, supported by infrastructure development and its growing role in traffic between central-eastern Europe and overseas markets. However, the question of service competitiveness and the ability to attract new direct routes in an increasingly volatile global context remains open.